.png)

NBFC vs MFI vs Fintech: What's the Difference, and Why It Matters

Get In Touch

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

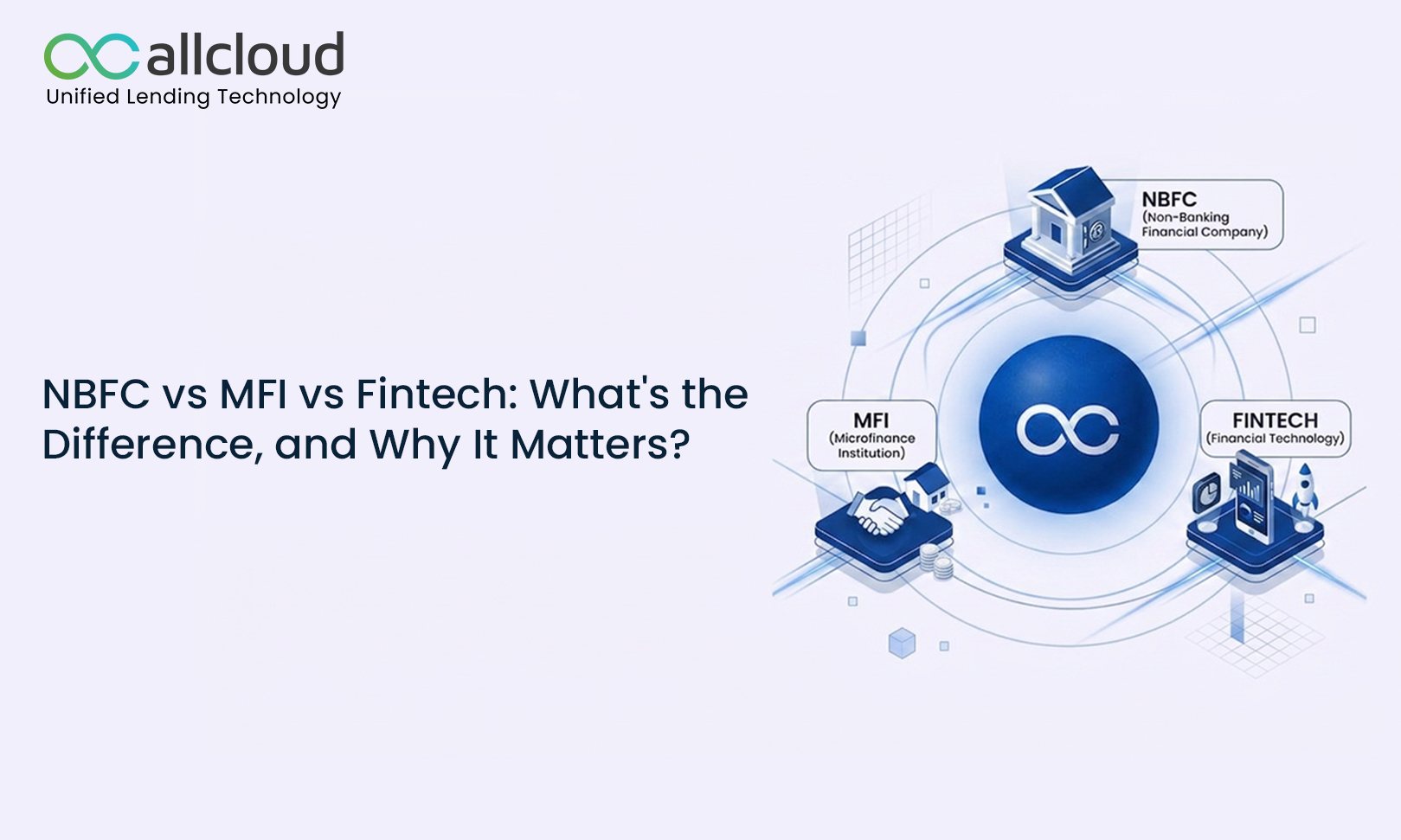

Spend any time around Indian lending circles and you'll hear "NBFC," "MFI," and "fintech" used almost interchangeably. That's a problem, because mixing them up leads to real confusion about who regulates whom, how each is funded, and critically, what kind of operational software each actually needs.

NBFC vs MFI: The Core Difference

A Microfinance Institution (MFI) is a narrower lending category typically focused on small-ticket loans to low-income borrowers, often delivered through group-lending or joint-liability models. An NBFC is the broader, RBI-registered umbrella category that can include MFIs alongside asset finance, housing finance, gold loan, and other lending business models. The regulatory ceilings on loan size, pricing, and borrower income eligibility differ meaningfully between a general NBFC and a microfinance-focused one.

NBFC vs NBFC-MFI: A Common Point of Confusion

This is the distinction that trips people up most often, because "NBFC-MFI" isn't a separate kind of company it's a defined RBI sub-category of NBFC. An entity becomes an NBFC-MFI by meeting specific qualifying criteria: a minimum percentage of its loan book in qualifying microfinance loans, income caps on borrowers, and pricing restrictions on loans extended. The practical takeaway: every NBFC-MFI is an NBFC, but not every NBFC is an NBFC-MFI and the compliance and reporting obligations differ accordingly.

Fintech vs NBFC: Technology Approach vs Regulatory License

NBFC is a license. Fintech is an approach to delivering financial services using technology it's not a regulatory category at all. A lot of consumer-facing "fintech lenders" you've encountered are, legally, NBFCs underneath the branding, or they operate through a partnership with one, because lending in India generally requires that license (or a bank tie-up) to function. The reverse is also increasingly common: traditional NBFCs adopting fintech-style operations digital onboarding, API-based underwriting, cloud-based loan management without changing their underlying license at all.

What Comes Under the NBFC Umbrella, Broadly?

Pulling the categories together, the RBI's classification of NBFCs spans:

- Asset finance companies

- Loan companies

- Investment companies

- Infrastructure finance companies

- Microfinance institutions (NBFC-MFIs)

- Housing finance companies

Each operates under its own specific regulatory sub-rules, even though all fall under the same overarching NBFC license structure.

Why the Category You Operate Under Changes Your Software Needs

This isn't just regulatory trivia it has direct operational consequences. An NBFC-MFI running group-lending models needs software built around joint-liability tracking and center-meeting workflows; a gold loan NBFC needs collateral valuation and pledge management; an MSME-focused NBFC needs cash-flow-based underwriting rather than just credit-bureau scoring. Generic, one-size-fits-all platforms tend to require workarounds exactly at the points where these category-specific workflows matter most which is usually where operational cost and compliance risk actually live.

FAQ

Is an NBFC-MFI different from a regular NBFC?

Yes, NBFC-MFI is a defined RBI sub-category requiring a minimum share of microfinance lending and specific borrower income limits; a general NBFC has no such restriction.

Are fintech companies regulated the same way as NBFCs?

Not directly, "fintech" isn't a regulatory category. Most fintech lenders either hold an NBFC license themselves or partner with a licensed NBFC or bank.

What types of companies fall under the NBFC category?

Asset finance, loan, investment, infrastructure finance, microfinance, and housing finance companies are the main NBFC sub-categories recognized by the RBI.

Does the type of NBFC affect what software it needs?

Yes, significantly, loan workflows, collateral handling, and compliance reporting differ by NBFC category, which is why configurable, category-aware platforms outperform generic accounting tools.